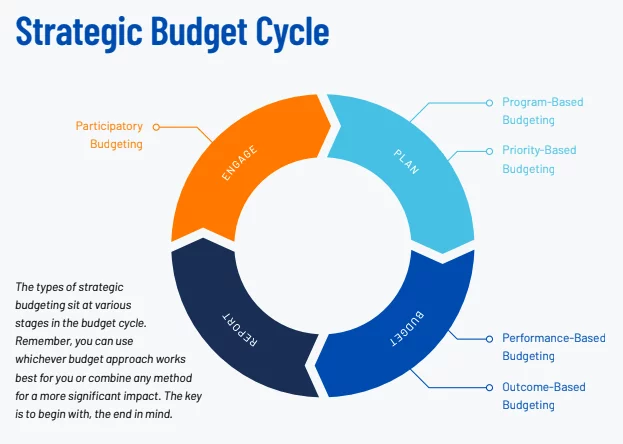

In the contemporary financial landscape, budget planning tips are crucial for managing both personal and business finances effectively. As economic uncertainties continue to challenge individuals and organizations alike, mastering the art of budgeting has never been more imperative. This comprehensive guide delves into advanced strategies and practical insights to enhance your budgeting acumen.

Understanding the Essence of Budget Planning

Budgeting, at its core, is not merely about tracking expenses; it is a strategic approach to financial management. Effective budget planning involves forecasting revenues and expenditures, setting financial goals, and adjusting your strategies in response to changing circumstances. With an increasing array of tools and methodologies available, it’s essential to adopt a method that aligns with your specific needs.

Establish Clear Financial Objectives

Before diving into the intricacies of budget planning tips, it’s vital to establish clear financial objectives. These objectives should be SMART—Specific, Measurable, Achievable, Relevant, and Time-bound. For instance, if you aim to save for a major purchase, define the amount needed, the timeframe, and the steps to reach this goal.

Define Your Goals

- Short-Term Goals: These might include saving for a vacation or paying off credit card debt.

- Medium-Term Goals: Consider saving for a down payment on a home or funding a child’s education.

- Long-Term Goals: These encompass retirement savings or building a substantial investment portfolio.

Implementing Effective Budgeting Techniques

Adopting effective budgeting techniques can significantly impact your financial stability. Below are some budget planning tips to consider:

1. Use the Zero-Based Budgeting Method

Zero-based budgeting (ZBB) is a technique where every dollar of your income is allocated to specific expenses, savings, or debt repayment. At the end of the month, your budget should “zero out,” meaning all income is accounted for. This method ensures meticulous control over expenditures and prevents overspending.

2. Incorporate the 50/30/20 Rule

The 50/30/20 rule is a straightforward budgeting approach:

- 50% of your income should be allocated to necessities such as housing, utilities, and groceries.

- 30% should be directed towards discretionary spending like entertainment and dining out.

- 20% is reserved for savings and debt repayment.

This rule provides a balanced framework for managing your finances while allowing for flexibility.

3. Utilize Budgeting Software and Apps

In the digital age, leveraging technology can streamline the budgeting process. Various budget planning tips involve using sophisticated software and apps to track expenses, set financial goals, and analyze spending patterns. Tools such as Mint, YNAB (You Need a Budget), and EveryDollar offer comprehensive features for efficient budget management.

Monitoring and Adjusting Your Budget

Regular monitoring and adjustment are crucial components of successful budgeting. Financial circumstances can fluctuate due to various factors such as income changes, unexpected expenses, or shifts in financial goals. Thus, periodic reviews and adjustments are necessary to maintain financial stability.

Track Your Spending

Consistent tracking of your spending habits helps identify areas where you may be overspending or where you can cut back. Detailed records of expenses can provide valuable insights into your financial behavior and enable you to make informed adjustments.

Review and Revise Your Budget Regularly

A static budget can become outdated quickly. Therefore, it’s essential to review and revise your budget regularly, especially when significant life events occur, such as a change in employment status or the birth of a child. This adaptability ensures that your budget remains relevant and effective.

Planning for the Unexpected

An integral part of budgeting involves preparing for unforeseen circumstances. Unexpected expenses, such as medical emergencies or vehicle repairs, can disrupt financial plans. Implementing strategies to manage these uncertainties is crucial for maintaining financial resilience.

Build an Emergency Fund

An emergency fund acts as a financial safety net during unforeseen circumstances. Aim to save at least three to six months’ worth of living expenses in a readily accessible account. This fund can help cover unexpected costs without derailing your budget.

Secure Adequate Insurance Coverage

Adequate insurance coverage, including health, auto, and home insurance, can mitigate the financial impact of unexpected events. Review your insurance policies regularly to ensure they provide sufficient coverage and make adjustments as necessary.

Leveraging Financial Insights for Strategic Decisions

Incorporating financial insights into your budgeting strategy can enhance decision-making and financial outcomes. Analyze spending patterns, investment performance, and savings growth to inform strategic decisions.

Conduct Financial Analysis

Regularly analyze your financial data to identify trends, patterns, and areas for improvement. Financial analysis tools and techniques can provide valuable insights into your financial health and guide strategic planning.

Set Up Financial Milestones

Setting financial milestones can provide motivation and a sense of achievement. Milestones might include reaching a savings target, reducing debt by a certain amount, or achieving a specific investment return. Celebrate these milestones to reinforce positive financial behaviors.

Conclusion

Navigating the complexities of personal and business finances requires a strategic approach to budgeting. Implementing the budget planning tips outlined in this guide can help you achieve financial stability and success. From setting clear financial goals to utilizing technology and preparing for the unexpected, these strategies are designed to enhance your budgeting proficiency and foster long-term financial well-being. For more insights on effective budget planning, visit Bandpaid, where you can explore additional resources and tools to optimize your financial management.