In the labyrinth of modern finance, understanding your credit score is crucial for navigating the complexities of personal and professional financial management. This numerical representation of creditworthiness plays a pivotal role in determining various aspects of one’s financial life, from loan approvals to interest rates. This comprehensive examination delves into what a credit score is, its significance, and the implications of maintaining a favorable credit score.

Understanding the Credit Score

Definition and Components

A credit score is a numerical value derived from an individual’s credit history, reflecting their creditworthiness. It is a critical metric used by lenders and financial institutions to evaluate the risk associated with lending money. This score is calculated based on several components, including:

- Credit History: A record of an individual’s credit accounts, including credit cards, loans, and mortgages, along with the payment history associated with these accounts.

- Credit Utilization: The ratio of current credit card balances to the credit limits, which indicates how much of their available credit a person is using.

- Length of Credit History: The duration for which an individual has maintained credit accounts. A longer credit history generally contributes to a higher credit score.

- Types of Credit Accounts: The variety of credit accounts, such as revolving credit (credit cards) and installment loans (car loans, mortgages), which can impact the score.

- Recent Credit Inquiries: The number of recent inquiries made by lenders or other entities into an individual’s credit report, which can affect the score.

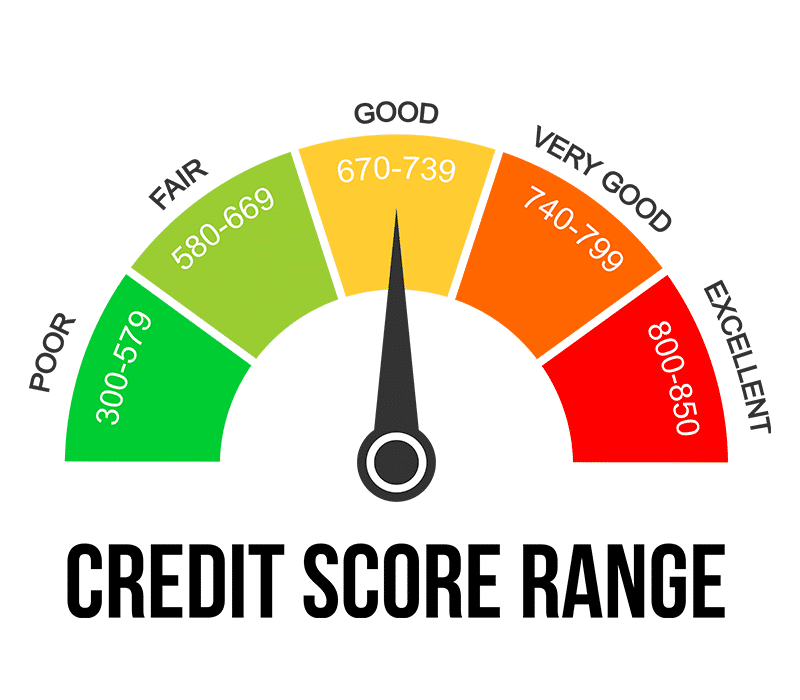

Credit Score Ranges

Credit scores typically fall within a range of 300 to 850, with higher scores indicating better creditworthiness. The ranges can be categorized as follows:

- Excellent (750 – 850): Individuals with scores in this range are considered highly creditworthy, often receiving the best terms on loans and credit cards.

- Good (700 – 749): This range indicates a strong credit history, with favorable interest rates and terms available.

- Fair (650 – 699): A score in this range suggests a need for improvement in credit management. Individuals may face higher interest rates and less favorable terms.

- Poor (600 – 649): A lower score indicates a higher risk for lenders, leading to more difficult borrowing conditions and higher interest rates.

- Very Poor (300 – 599): Individuals with scores in this range may struggle to obtain credit or face very high interest rates.

The Importance of a Credit Score

Financial Implications

Understanding what a credit score is and its implications is essential for effective financial management. A high credit score can lead to several financial benefits, including:

- Favorable Loan Terms: Individuals with higher credit scores are more likely to qualify for loans with lower interest rates, reducing the overall cost of borrowing.

- Easier Credit Approval: A good credit score increases the likelihood of approval for credit cards, loans, and mortgages, making it easier to access credit.

- Lower Insurance Premiums: Some insurance companies use credit scores to determine premiums, with higher scores potentially leading to lower rates.

- Better Rental Opportunities: Landlords often review credit scores as part of the rental application process. A high credit score can enhance rental approval chances.

Impact on Financial Opportunities

A credit score also influences various other aspects of financial opportunities:

- Employment Opportunities: Some employers review credit scores as part of the hiring process, particularly for positions involving financial responsibilities.

- Security Deposits: Utility companies and service providers may require lower security deposits from individuals with higher credit scores.

- Negotiation Leverage: A strong credit score provides leverage in negotiating terms for loans, credit cards, and other financial agreements.

Factors Affecting Credit Scores

Payment History

One of the most significant factors affecting a credit score is payment history. Consistent, timely payments on credit accounts contribute positively to the score, while late payments, defaults, or bankruptcies can significantly damage it.

Credit Utilization Ratio

The credit utilization ratio, which is the proportion of credit used relative to the available credit limit, plays a critical role. Maintaining a low utilization ratio—generally below 30%—is favorable for the credit score.

Length of Credit History

The length of the credit history contributes to the credit score. Longer credit histories provide more data for assessing creditworthiness, typically resulting in a higher score. Closing old accounts can negatively impact this aspect of the score.

Types of Credit Accounts

Diverse credit types, such as a mix of credit cards, installment loans, and retail accounts, can positively influence the credit score. This diversity demonstrates the ability to manage various forms of credit responsibly.

Recent Credit Inquiries

Frequent inquiries into an individual’s credit report can impact the score. Hard inquiries, made by lenders during the loan application process, can cause temporary dips in the credit score.

Strategies for Improving and Maintaining a Good Credit Score

Timely Payments

Consistently making timely payments on all credit accounts is fundamental to maintaining a good credit score. Setting up automatic payments or reminders can help ensure that payments are never missed.

Managing Credit Utilization

To manage credit utilization, aim to keep the balance on credit cards well below the credit limit. Paying off balances in full each month or maintaining low balances relative to the credit limit is advisable.

Maintaining a Long Credit History

Keeping older credit accounts open can benefit the length of credit history. Even if accounts are not actively used, maintaining them can positively impact the credit score.

Diversifying Credit Types

Having a mix of different credit types, such as revolving credit and installment loans, can be beneficial. However, it is crucial to manage all credit accounts responsibly to maintain a high credit score.

Minimizing Hard Inquiries

Minimize the number of hard inquiries by avoiding multiple loan or credit applications in a short period. When shopping for loans, limit inquiries to a specific time frame to reduce the impact on the credit score.

Common Misconceptions About Credit Scores

Myths and Facts

Several myths surround what a credit score is and its impact. Clarifying these misconceptions can aid in effective credit management:

- Myth: Checking your own credit report lowers your score.

- Fact: Checking your own credit report is considered a soft inquiry and does not affect your score.

- Myth: Closing old credit accounts improves your score.

- Fact: Closing old accounts can reduce the length of your credit history and potentially harm your score.

- Myth: Paying off a debt will immediately improve your score.

- Fact: While paying off debt is beneficial, improvements to the credit score may take time to reflect in credit reports.

- Myth: A good credit score guarantees loan approval.

- Fact: While a good credit score improves the chances of approval, other factors such as income and debt-to-income ratio are also considered.

Resources for Credit Score Management

Online Tools and Platforms

Various online tools and platforms can assist in managing and monitoring your credit score:

- bandpaid.com: Explore resources and tools available on bandpaid.com to gain insights into credit management and access services designed to help improve and monitor your credit score.

- Credit Monitoring Services: Utilize credit monitoring services to track changes in your credit report and receive alerts for potential issues.

Professional Assistance

- Credit Counseling: Seek advice from credit counseling agencies for personalized guidance on managing credit and improving your score.

- Financial Advisors: Consult financial advisors for comprehensive financial planning, including strategies to enhance creditworthiness and overall financial health.

Conclusion

Understanding what a credit score is and why it matters is essential for making informed financial decisions and achieving long-term financial stability. By comprehending the factors that influence your credit score and employing effective strategies for management and improvement, you can enhance your creditworthiness and secure better financial opportunities.

Maintaining a good credit score involves diligent financial management, including timely payments, responsible credit utilization, and strategic planning. For additional resources and tools to assist with credit score management, visit bandpaid.com to explore options designed to support your financial journey.